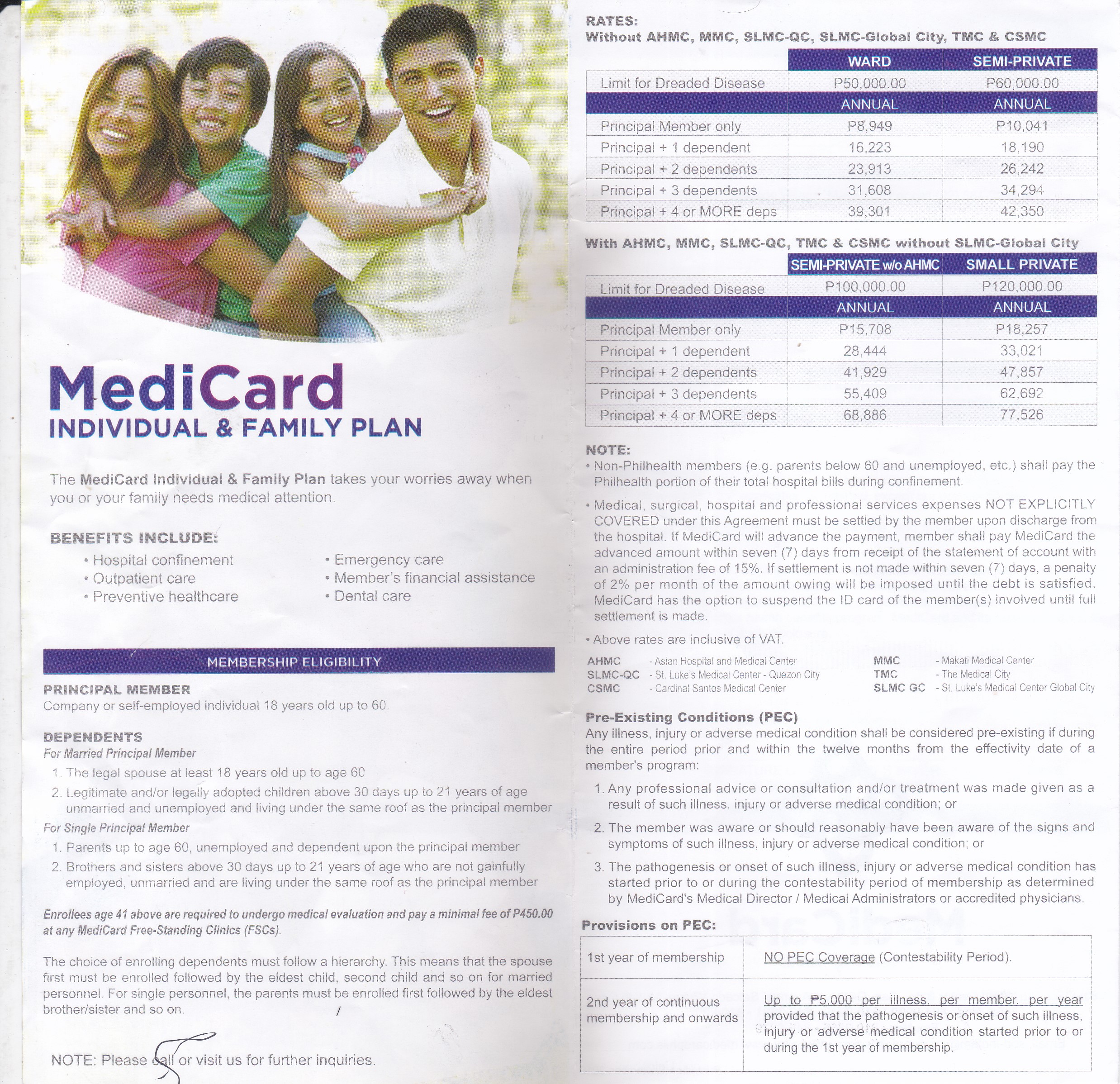

Getting sick in the Philippines is very expensive especially if you don’t have money and health insurance. Many Filipinos are forced to borrow money from the bank, friends and relatives just to pay piling medical bills. Health emergencies also eat up savings and even investments. Of course Philhealth is there, but it will not pay everything especially when you are confined in private hospitals. Philhealth can only pay a percentage of the total bill. Philhealth cannot also be used for outpatient services (check-ups) and for dental services.

HMO stands for Health Maintenance Organization, which is a business that provides customers with access to a full range of medical facilities at their time of need, in exchange for membership fees up front. There are 16 HMOs in the market today including Medicard, Maxicare, Intellicare, Fortunecare, Valucare, Philcare, Insularcare and others. HMO plans typically cover inpatient, outpatient, and emergency room treatments. Members can avail of a host of services from among a nationwide network of accredited doctors, hospitals and clinics, and on a no-cash-out basis. In most cases, members need only show their health cards to avail of the services.

I personally use my HMO card for medical check-ups and I don’t need to pay anything. I can use my card for unlimited check-ups as long as the illness is covered. I also use my card for dental check ups and get free dental filling (pasta in Tagalog). My card also cover a free annual medical exam with chest Xray, urinalysis, faecalysis, blood chemistry and physical exam.

When confined, the HMO card will pay the bill after the Philhealth coverage has been lessened. If you do not have Philhealth, you need to pay the portion of the bill that Philhealth should have been covered if you are Philhealth member. You will appreciate the value of an HMO card if your medical bill would be like 50,000 or higher. Imagine, the feeling of leaving the hospital without paying huge amount of money.